Interested in seeing a demo?

Fill out the following information (please ensure you provide some detail on the problem you are looking to solve or the Messagepoint product you are interested in).

This webinar, hosted by the Mortgage Bankers Association, brings together leaders from Messagepoint and Newbold Advisors to examine how mortgage servicers can modernize borrower communications to keep pace with changing expectations and regulatory demands. The panel features:

Together, they outline the persistent issues mortgage servicers face in managing their borrower communications and the best practices that can help overcome them.

Below is a high-level summary of the discussion:

Mortgage servicers today are under growing pressure to improve their borrower communications. From state regulatory bodies tightening oversight, to consumers expecting faster, more personalized experiences, the environment has shifted dramatically.

“There are always changes coming around in how regulators want you to communicate with the consumer,” Duwaine explained. “And they’re always putting a very tight timeline on the servicer to get communications updated quickly and in place.”

Consumer expectations have also evolved. As Patrick noted, “97% of adults under 65 use a smartphone. Even in the over-65 category, it’s 76%. Borrowers now expect the same digital experience from their servicer that they get from Amazon or Google.”

Despite these pressing dynamics, many servicers still rely on outdated systems and rely heavily on third party print servicer providers which inhibit the speed of managing borrower communications. Manual workflows, scattered review processes, and weeks-long turnaround times remain the norm—even for basic changes. As a result, borrower communications processes are slow, inefficient, and costly. In addition, they are blocking innovation and digital transformation of the borrower experience. To break that cycle, the panel introduced three best practices every servicer should adopt.

Too many servicers remain dependent on third-party service providers (PSPs) for even the smallest changes to borrower communications. That means waiting in line behind larger clients, managing change requests through long email threads, and enduring approval cycles that delay updates that should take hours.

As Duwaine Thomas of Newbold Advisors explained during the webinar, “We were often held hostage by our print providers, waiting weeks for simple updates—like modifying a footer or rewording a paragraph to be clearer.”

Bringing content and communication management in-house gives servicers the ability to act faster. It means updates can be made in hours—not weeks—and servicers can avoid vendor lock-in by easily redirecting output across different channels or providers. “It’s a huge game changer,” Duwaine noted. “Not just making changes quickly, but with the right controls in place to ensure that Legal, Risk, and Compliance have all reviewed and approved those changes before they go out the door.”

Modern borrower communications platforms eliminate the need for IT to code templates or handle rule logic. With intuitive, no-code tools, content owners can author, test, and approve updates in a single interface—dramatically shortening cycles and minimizing rework.

Patrick Kehoe emphasized this point: “If you empower your business teams with a solution that doesn’t require coding… you can change your mind, test iteratively, and reduce time and cost from days and weeks to hours and minutes”.

In legacy systems, there’s a separate template library for every state, brand, or product—This creates massive duplication and risk. A modern solution that uses intelligent variation management to address this complexity head-on.

“You might have Texas or Florida receiving the same content, but we all know California and New York will require something unique,” said Patrick. By storing all these variants in a single content object and applying them automatically based on business rules, servicers eliminate redundancy and simplify change management.

A modular approach allows content to be created once and reused across multiple communications and even across channels. Reusable blocks—like payment instructions or hardship language—are stored centrally and applied wherever needed. Updates are made in one place and flow automatically across all relevant communications. This significantly reduces maintenance and ensures consistency across touchpoints.

One top-five mortgage servicer who implemented these best practices transformed cut its change cycles from 4–6 weeks to just one day. They also saved $50,000 in fees typically paid to their service provider for changes, controlling the spend more efficiently using in-house resources.

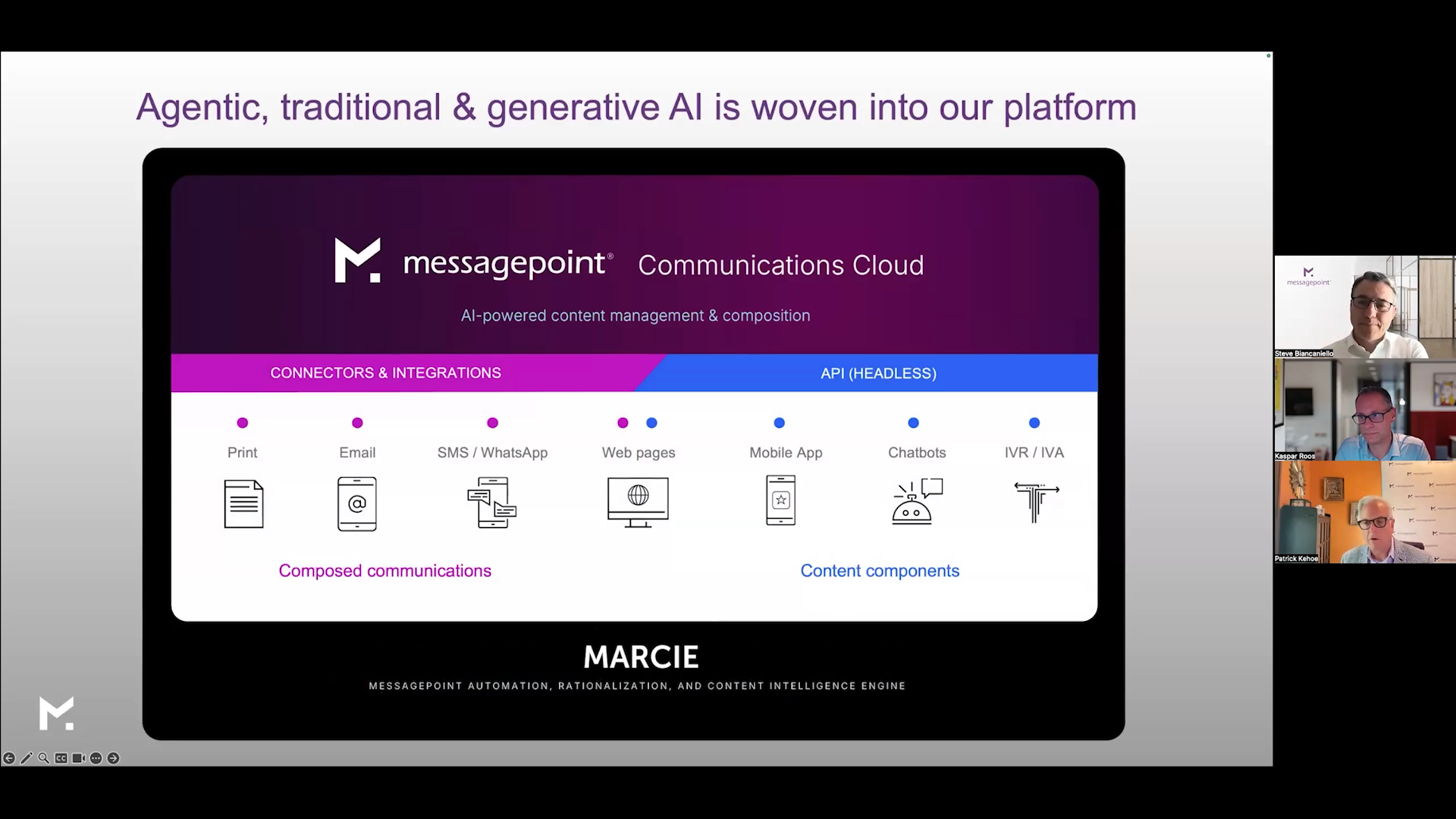

To embrace digital transformation, servicers must centralize content management and decouple content from delivery format. That means storing content in one place and using it flexibly across email, SMS, mobile apps, web portals, and print.

The COPE (Create Once, Publish Everywhere) and CORE (Create Once, Repurpose Everywhere) frameworks—discussed in the session—enable this. Content is created once, and adapted for different formats and channels without duplication. Shortened versions for mobile, longer versions for print, and ADA-compliant digital formats are all derived from the same content foundation.

As Patrick explained, “You’re not managing multiple versions across different teams. You’ve got one place where content lives, and that content drives everything that goes out.”

This centralization streamlines governance and speeds up production. It also ensures consistency across borrower touchpoints—reducing confusion, call volume, and risk. Duwaine added, “It’s not just about being fast. It’s about being consistent across all the places a borrower may see that information.”

Borrower communications need to be easily understood across reading levels, languages, and channels. The CFPB and other regulators are placing greater emphasis on plain language, especially for Limited English Proficiency (LEP) borrowers. “Nearly 48% of adults in the U.S. read below a sixth-grade level,” Patrick noted. “That makes readability and comprehension a huge issue for mortgage servicers”.

Unclear communications not only increase regulatory risk, they can cause increase borrower confusion leading to adverse outcomes and added call center volume.

To meet these demands, servicers are increasingly turning to generative AI tools—not to replace humans, but to support them in rewriting complex content, simplifying technical language, and generating translations that are accurate and accessible.

Patrick emphasized the role of AI as an assistive tool: “AI is a support mechanism. It helps you rewrite content to a fifth-grade level. It helps you translate. It helps you summarize. But people are still in control”.

By combining AI-generated suggestions with human review and institutional knowledge, teams can improve clarity without sacrificing compliance. Organizations hesitant about AI often change their minds after seeing the benefits of AI and automation. Rewriting content for clarity, translating it accurately, and summarizing it for digital use are now exponentially faster. Real metrics show that optimization is 14x faster, translation is 20x faster, and summarization is 5x faster.

This is just a preview of the insights shared in this webinar. Complete the form above to watch the full recording.

Agentic AI is transforming the landscape of customer communications management. Watch now to learn what that means, and…

Watch the video

TORONTO, June 25, 2026 – Messagepoint, a leading customer communications management (CCM) solutions provider, today announced that MARCIEAssure™…

Read more

Messagepoint was recognized as a Leader in the 2026 Aspire CCM-CXM Technology Vendors Leaderboard for the eighth consecutive…

Read the whitepaper