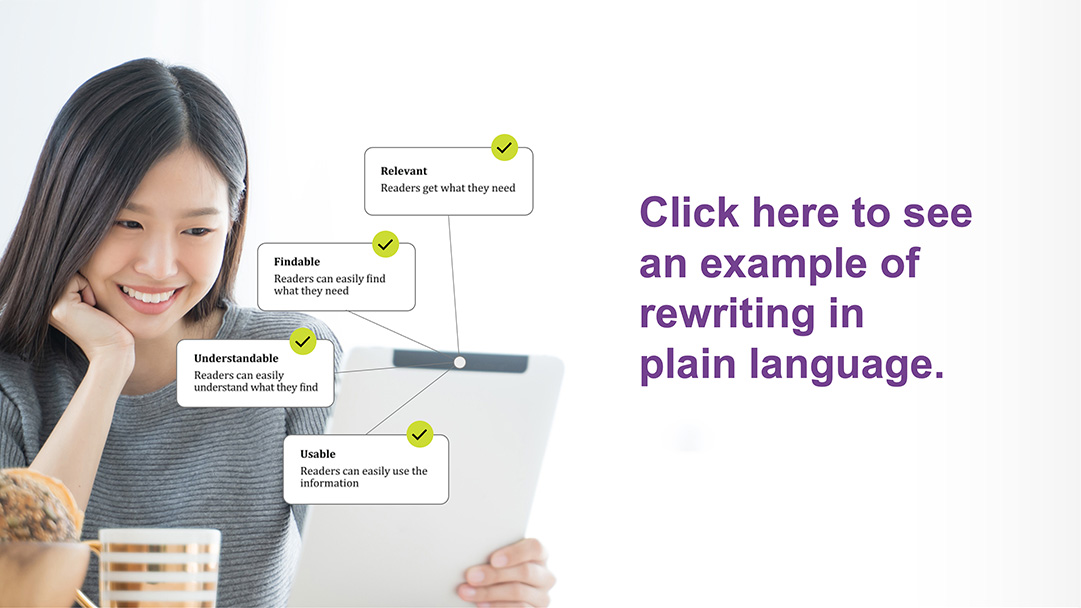

Clear, concise borrower communications are essential for effectively supporting borrowers and enabling confident financial decisions.

Unfortunately, most mortgage servicing communications are filled with complex phrasing, legalese, and mortgage industry jargon, as a result of being authored or edited by legal teams that prioritize compliance over clarity. Considering more than half of U.S. citizens read below the equivalent of a sixth-grade level and that 25.6 million have limited English proficiency, most mortgage servicers simply aren’t doing enough to meet borrowers where they are at. During default and loss mitigation when the volume and complexity of communications increase, this can lead to more calls to the call center, misunderstandings about next steps, and confusion about what options even exist. In these situations, it’s vital that borrowers understand their options to take the appropriate steps to avoid losing their homes.

Recognizing this problem, the CFPB requires that borrower communications be “clear and conspicuous”. While the CFPB hasn’t provided detailed guidelines on how to meet this standard, they do recommend servicers use “plain language” as much as possible in their communications.

In this blog, we’ll explore what plain language writing is, how it improves borrower understanding, and how to use generative AI to implement it efficiently.

Plain language writing aims to make communications clear and accessible to a broader audience. This concept originated in the 1970s when government organizations sought to simplify regulations to address communication issues. Advocates have continued to promote plain language for its effectiveness in helping consumers understand complex topics, such as those common in mortgage servicing.

In June 2023, the International Organization for Standardization (ISO) released principles and guidelines on adopting plain language for text-based communications and documents. From a borrower communications perspective, the relevant best practices include:

Although mortgage servicers recognize the importance of clear communications and aspire to meet plain language standards, legacy technologies for managing borrower communications make updating content very costly and time-consuming due to the highly manual processes involved. Content authors must painstakingly comb through hundreds of documents and templates, one by one, to identify and correct offending content. Even if a servicer manages to bring all their content up to an acceptable standard of plain language, issues re-emerge without tools to maintain content standards over time.

Generative AI platforms such as ChatGPT can be leveraged to rewrite borrower communications that embody plain language principles. However, leveraging AI successfully and efficiently requires the right knowledge and approach.

Success starts with prompt engineering. Prompt engineering is the practice of writing instructions that you give to a generative AI engine to achieve a desired outcome. It’s helpful to think of generative AI like a new junior employee in your organization. They may be smart and capable but lack detailed knowledge of your industry and your business’ standards and practices. Like this employee, generative AI tools will require specific guidance before they can accurately produce the desired outcome. This guidance is called a prompt. The complex nature of plain language writing and the need for accuracy in borrower communications makes this a tricky process that requires knowledge of plain language principles, borrower communication requirements, and your business.

While this sounds like a big undertaking, modern customer communications management (CCM) systems offer servicers the opportunity to leverage generative AI in a more controlled way, from within the same environment where customer communications are managed. Key things to look for include:

67.8 million Americans speak a language other than English at home. For these customers, having communications in their preferred language is critical. In the same way that plain language principles will enable servicers to better support English speakers, translating communications can make all the difference in enabling borrowers to understand their options. In fact, the CFPB has turned their lens toward LEP consumers to determine how financial services organizations can better support these populations. Generative AI translation capabilities are a game-changer, producing high-quality translations 20 times faster than humans, and accuracy checks to validate the meaning and structure are consistent across all language versions.

Generative AI presents a unique opportunity for mortgage servicers to reduce calls to the call center and better support their borrowers by making it easier to improve the quality of borrower communications across all channels. The safest and most effective way to take advantage of this is through integration with your borrower communications management system. As the generative AI landscape continues to evolve rapidly, you can rest assured that your vendor will identify innovative and applicable use cases, enabling your organization to maintain a competitive edge.